A software executive with a $250,000 salary buys a short term rental. A cost segregation study and first-year depreciation throw off a $120,000 paper loss. Because the property qualifies under one specific rule, that loss is not passive. It offsets her W-2 income, and her tax bill drops by tens of thousands of dollars.

That is the short term rental tax loophole. It is one of the few ways a high earner can use real estate losses against active income without quitting their job to qualify. Here is how it works, what it takes to earn it, and the catches.

What is the short term rental tax loophole?

The short term rental tax loophole lets owners deduct rental losses against W-2 or active business income. It works because a property with an average guest stay of seven days or fewer is not treated as a passive "rental activity" under the tax code. If the owner materially participates, meaning they are actively involved in running the rental, the losses become non-passive and offset active income, with no real estate professional status required.

That last part is what makes it powerful. Normal rental losses are passive. They can only offset passive income, and they sit on a shelf as carryforwards until you sell or until you have passive gains to absorb them. A high earner with mostly W-2 income gets no current benefit. The short term rental rules change that result.

Why short term rentals escape the passive-loss trap

Rental real estate is passive by default under Section 469 of the Internal Revenue Code. That is the rule that traps most landlords. To get out, you normally have to qualify as a real estate professional, which requires more than 750 hours and more than half your working time in real estate. Most people with a day job cannot meet it.

Short term rentals get out a different way. Under Treasury Regulation 1.469-1T(e)(3)(ii)(A), an activity is not a "rental activity" at all when the average period of customer use is seven days or fewer. No rental activity means the automatic passive rule never attaches. You are left with an ordinary trade or business, and the only question is whether you materially participate in it.

Long-term rental

- Passive by default

- Needs real estate professional status to offset W-2 income

- Rarely realistic while holding a full-time job

At tax time

Losses usually sit idle. They cannot touch your salary.

Short term rental · avg stay 7 days or fewer

- Not a "rental activity" at all

- Only needs material participation, no special status

- Often realistic while keeping your day job

At tax time

Losses can offset your W-2 income.

The seven-day test looks at the average, not every single stay. Run the math on your actual booking data. A property with mostly two- and three-night stays clears it easily. One that drifts toward monthly bookings may not.

How do you prove material participation?

Material participation is the part you have to earn, and it is where the IRS pushes back. There are seven tests, and you only need to meet one. Two matter for most owners:

- The 500-hour test. You spend more than 500 hours working on the short term rental during the year. This test has no comparison to anyone else. Your 500 hours stand on their own.

- The 100-hour test. You spend more than 100 hours working on the short term rental, and more than any other single person involved. This one is a comparison, and it is where a paid manager or cleaner can knock you out.

Hours that count include guest communication, setting and adjusting pricing, coordinating maintenance and turnovers, managing the listing, bookkeeping for the property, and planning improvements. Time spent purely as an investor, like reviewing financial statements or researching your next purchase, does not count.

The documentation standard is strict. The IRS expects a contemporaneous log, meaning you record hours as you go, not a number you reconstruct from memory the night before an audit. A calendar, a time-tracking app, or a simple spreadsheet kept through the year is the difference between a defensible position and a disallowed one.

One more trap to know. Personal use of the property is limited. If you use it yourself for more than 14 days, or more than 10% of the days it is rented, the property can fall under the vacation-home rules and lose this treatment. Keep your own stays short and documented.

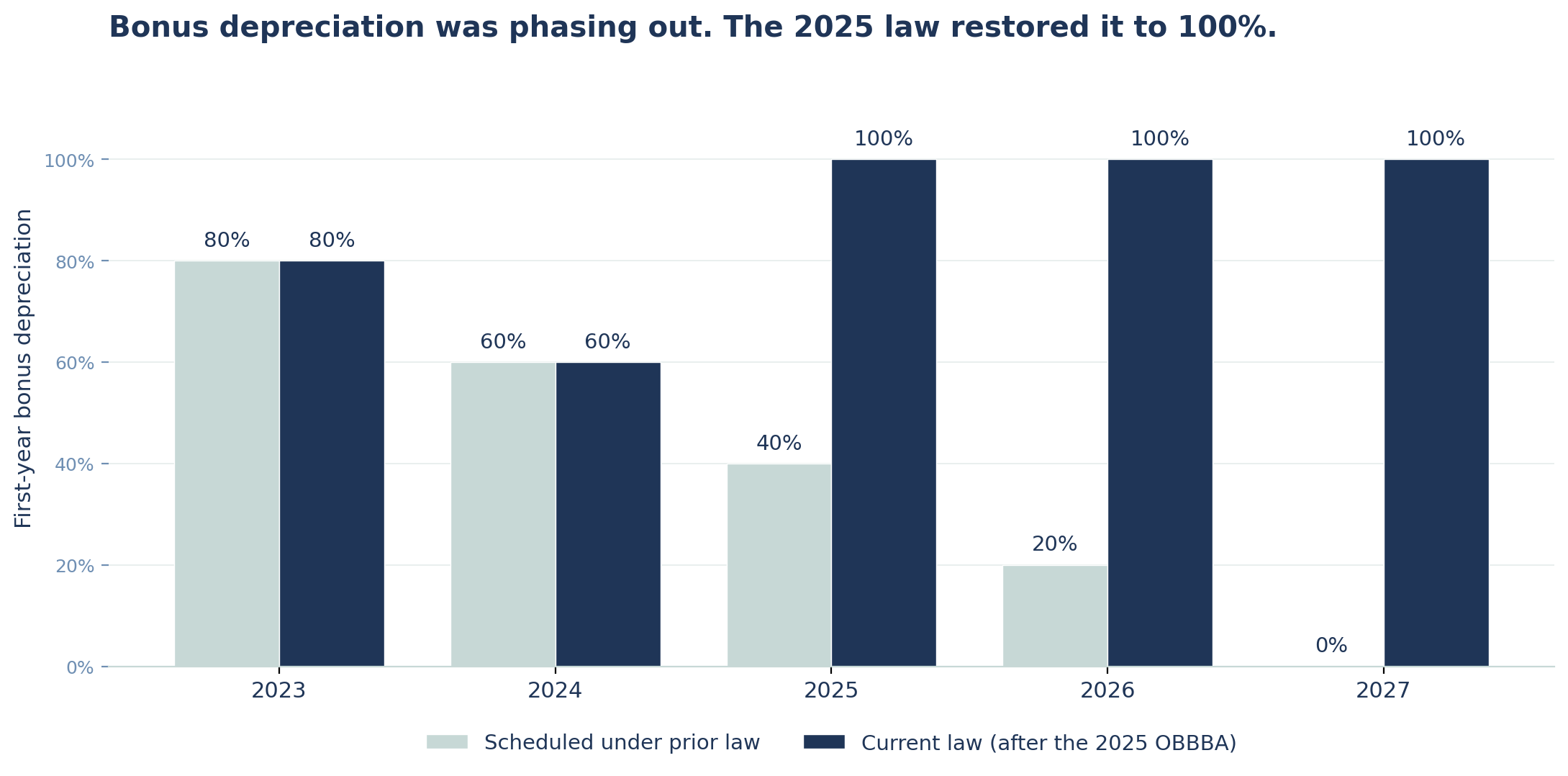

Is 100% bonus depreciation back in 2026?

Yes, and this is the part that makes 2026 a notable year to buy. The loss itself usually comes from depreciation, accelerated by a cost segregation study.

A cost segregation study breaks a property into its components. Instead of depreciating the whole building over 27.5 years, an engineering-based study reclassifies roughly 20% to 30% of the purchase price into 5-, 7-, and 15-year property: things like flooring, appliances, cabinetry, landscaping, and fixtures. Those shorter-life assets are eligible for bonus depreciation, which lets you deduct their full cost in year one.

Bonus depreciation was phasing out. Under the prior schedule it dropped to 60% in 2024, 40% in 2025, and was set to fall to 20% in 2026. The One Big Beautiful Bill Act, signed July 4, 2025, reversed that. It permanently restored 100% bonus depreciation for qualifying property acquired after January 19, 2025, per IRS Notice 2026-11. So a property you buy and place in service now can write off the full reclassified amount immediately, instead of the 20% the old law would have allowed.

A rough, illustrative example. On a $750,000 short term rental, a cost segregation study might move $160,000 to $200,000 into short-life property. With 100% bonus depreciation, that entire amount becomes a first-year deduction. Stack it on top of normal operating expenses and you can produce a sizable paper loss in year one, even on a property that cash-flows. Your actual numbers depend on the building, the land allocation, and the study itself. Treat this as a sketch, not a quote.

Does hiring a property manager kill the loophole?

No. This is the most common myth about the strategy, and it is wrong.

The confusion comes from the 100-hour test, where a paid manager logging more hours than you does end that specific path. But the 500-hour test has no such comparison. If you put in more than 500 of your own hours, it does not matter how many hours your manager, cleaner, or co-host logs. You qualify on your own record.

So the real question is not "manager or no manager." It is "which test am I using, and can I document it." Plenty of owners stay genuinely involved in the parts that count, pricing strategy, vendor decisions, guest-experience standards, and capital improvements, while handing off the operational grind. Done right, professional management actually protects the position. We keep the booking records, turnover logs, and vendor history that substantiate your involvement, and a clean paper trail is exactly what survives an audit.

What we do not do is make you qualify. Your hours are your hours. We can tell you what we see owners do and keep the records straight, but the participation test is yours to meet, and your CPA should confirm the approach before you file. It is the same honesty we bring to what short term rental management actually costs.

See what the property could earn first

Before the tax math matters, the income has to pencil out. We run free revenue estimates on Florida short term rentals using real market data, so you can model the deal before you buy. Get a free revenue estimate.

Real estate agents:

Free Florida revenue estimates and STR feasibility checks for your buyer clients. Learn more about our agent program.

Is this strategy right for your situation?

The loophole rewards a specific profile: a high active income to offset, a property that genuinely books short stays, real hours to put in, and a long enough hold to make the math work. A few things to weigh before you count the savings:

- Carryforwards still apply if you fall short. Miss material participation in a given year and the loss does not vanish, but it goes passive and waits, the same shelf long-term landlords sit on. The benefit is timing, and timing only helps if you qualify in the year you need it.

- Depreciation comes back on sale. Accelerating deductions now means depreciation recapture later, taxed up to 25% on the building portion when you sell. A 1031 exchange can defer it. This is a shift in timing and rate, not free money, so model the exit, not just the entry.

- It is property by property, year by year. Each property stands on its own facts and its own log.

None of this is a reason to skip the strategy. It is a reason to run it with a CPA who does this work, with clean records from day one. If you would rather hand off the operational side and keep clean documentation without doing it yourself, that is exactly what our full-service short term rental management covers.

Frequently asked questions

Do I need real estate professional status to use the short term rental loophole?

No. Real estate professional status is the path for long-term rentals. Short term rentals with an average guest stay of seven days or fewer are not treated as rental activities under Treasury Regulation 1.469-1T(e)(3)(ii)(A), so you only need to meet one of the material participation tests instead. Confirm your specific facts with your CPA.

Can I still claim the loophole if I hire a property manager?

Yes, in most cases. A property manager only closes the 100-hour test, which compares your hours to everyone else's. The 500-hour test has no comparison, so documenting more than 500 of your own hours working on the short term rental qualifies you regardless of who else works on the property. Talk to your CPA about which test fits your situation.

What if my average guest stay is longer than seven days?

Then the property is treated as a normal rental activity and this treatment does not apply. There is a separate rule for an average stay of 30 days or fewer with significant personal services, but the clean version of the loophole runs on the seven-day-or-fewer average. Check your actual booking data before you rely on it.

Can I do a cost segregation study on a property I already own?

Yes. You can apply a cost segregation study to a property placed in service in a prior year and catch up the missed depreciation without amending old returns, using a change in accounting method. Your CPA handles the mechanics and confirms whether the savings justify the cost of the study.

This post is general information, not tax or legal advice. Tax outcomes depend on your specific facts, and the rules change. Confirm any strategy with a licensed CPA before you act on it.